.png?width=1050&height=450&name=email%20signature%20(4).png "email signature (4)")

Many companies do not keep claims information internally. They simply defer this record-keeping process to their insurance provider. However, there are several benefits to tracking this data in-house.

While it may be a bit of an adjustment at the start, you will quickly see a return on your investment as your risk management department and your organization as a whole benefits.

4 Reasons to Track Claims In-House

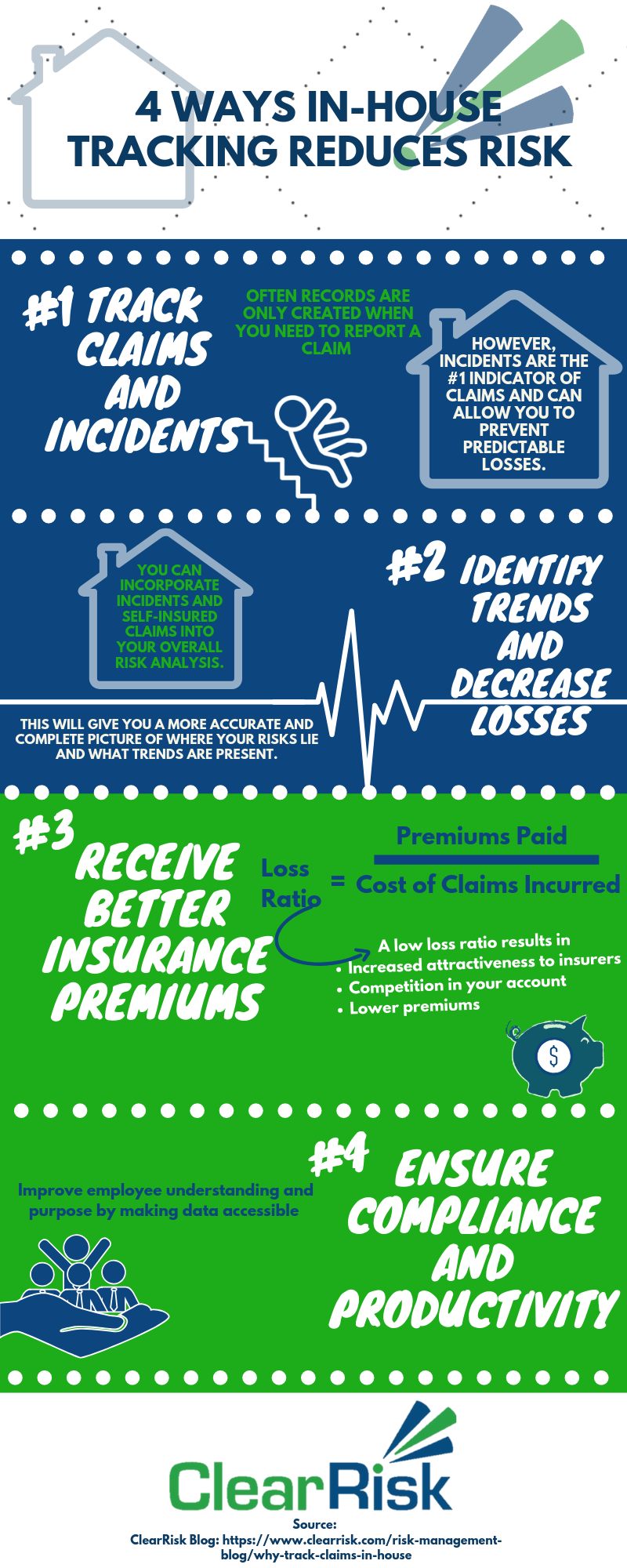

1. Track incidents as well as claims

If you don’t record or manage information in-house, it is likely that records are only created when you need to report a claim to your insurance provider. This means that you will only gather data on claims, where a formal case is brought against you, and not incidents.

However, incidents are the number one indicator of claims and can allow you to prevent predictable losses.

2. Identify trends and decrease losses

Having ownership of claims data means you can incorporate incidents and self-insured claims into your overall risk analysis. This will give you a more accurate and complete picture of where your risks lie and what trends are present.

For example, if ten people slip on your front step and you only record the one who tries to sue you, you would have no idea that there was historical data that could have predicted and prevented this outcome. With this tactic, you can better identify issues before they become claims and implement proper mitigation techniques, making occurrences less frequent and less severe.

Without tracking information in-house, this type of analysis is impossible.

3. Receive better insurance premiums

Insurance companies want to insure businesses that have “good” risk – those that they feel will have a minimum amount of losses.

A loss ratio is the premium paid divided by the cost of claims incurred. A low loss ratio will make your company attractive to insurers, which will result in competition over your account and lower premiums. Also, managing claims in-house will allow you to raise your deductible to the optimum level. The general principle is: the higher the deductible, the lower the premium.

By analyzing past losses in conjunction with insurance premium quotes for different deductible options, it becomes clear which deductible is best. If you raise this amount and agree to pay a higher portion of claim costs, the insurer will provide a discount on the premium payments in return.

Assuming you are financially able to pay this higher deductible, this strategy will save you money in the long run as the monthly savings will likely outweigh the higher cost if an accident occurs.

For more information on how strategically raising your deductible lowers premiums and saves your company money, check out this article. Internally handling claims data also means that you will have a complete and accurate record of losses if you decide to switch insurance providers.

4. Ensure compliance and productivity

It will be easier for your employees to understand the purpose and benefits of risk management practices if data is easily accessible. Compiling data and reports will be less time-consuming, as you will not have to rely on anyone but your internal risk management team.

Employees in other departments may also be more comfortable working with people within your company than those from an external insurance provider.

If you’d like to take advantage of the benefits that tracking claims and incidents data internally can bring, ClearRisk can help. Our Risk Management Information System is fully customizable and cloud-based, so data can be entered and tracked from anywhere into categories that suit your unique organization. We also offer full data migration, so you can import your historical data and use it instantly to start discovering trends and reducing losses. Your risk management department will thank you! Want more information? Learn more below.

If you found this article helpful, you may be interested in:

Your comments are welcome.